Data science project can be a challenging but rewarding process. By following the steps we can use in this blog, you can work through the project in an organized and effective way, and ultimately arrive at a solution to your problem.

Previously, we wrote blogs on many machine learning algorithms (Classification, Predication) as well as many other topics to help you sharpen your knowledge of how machine work. Please kindly visit our site and we would be happy if we got some feedback from you to improve our writing. To see some of them, you can follow the mentioned links.

Dataset is from Kaggle. This is the bank dataset for Credit evaluation whether to grant loan or not.

https://www.kaggle.com/datasets/brycecf/give-me-some-credit-dataset

Disclaimer: This exercise is targeted to audience of all levels including the beginners, so we will be using simple methods, not advanced functions.Some of concept in this blog are borrowed from lecture note of Data Scientist Nirmal Budhathoki.

Our goal: </br> For this notebook, we want to perform Exploratory Data Analysis (EDA), learn some data cleaning techniques, handling missing values and etc.

Business Understanding: For the banks, customers going to delinquent or default is a bad news. These are people who are not able to pay their credit. The defaulted loans goes to collection team. This is a loss for bank. Therefore, if we can predict whether a customer will default in next 90 days, then bank can take precautionary actions like interest relief, lower payment plan, extending payoff time etc.

Importing Required Libraries

import pandas as pd

import numpy as np

import joblib

import matplotlib.pyplot as plt

import seaborn as sns

%matplotlib inline

from IPython.display import Image

import warnings

from sklearn.linear_model import LogisticRegression

from sklearn.ensemble import RandomForestClassifier

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

from sklearn import metrics

from sklearn.metrics import confusion_matrix, classification_report, precision_recall_curve,recall_score

warnings.filterwarnings('ignore')

sns.set(rc={'figure.figsize':(10,8)})

Data Understanding: </br> Loading Data - We will only load training data for this exercise. You have to download the cs-training.csv from the above link and upload the file into you Google Drive. You can also use the API to read it from kaggle directly. More information on API in this link: https://www.kaggle.com/general/74235

## For now we will load from the drive

dataset = pd.read_csv('cs-training.csv')

## Checking top 5 rows

dataset.head()

| Unnamed: 0 | SeriousDlqin2yrs | RevolvingUtilizationOfUnsecuredLines | age | NumberOfTime30-59DaysPastDueNotWorse | DebtRatio | MonthlyIncome | NumberOfOpenCreditLinesAndLoans | NumberOfTimes90DaysLate | NumberRealEstateLoansOrLines | NumberOfTime60-89DaysPastDueNotWorse | NumberOfDependents | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 1 | 0.766127 | 45 | 2 | 0.802982 | 9120.0 | 13 | 0 | 6 | 0 | 2.0 |

| 1 | 2 | 0 | 0.957151 | 40 | 0 | 0.121876 | 2600.0 | 4 | 0 | 0 | 0 | 1.0 |

| 2 | 3 | 0 | 0.658180 | 38 | 1 | 0.085113 | 3042.0 | 2 | 1 | 0 | 0 | 0.0 |

| 3 | 4 | 0 | 0.233810 | 30 | 0 | 0.036050 | 3300.0 | 5 | 0 | 0 | 0 | 0.0 |

| 4 | 5 | 0 | 0.907239 | 49 | 1 | 0.024926 | 63588.0 | 7 | 0 | 1 | 0 | 0.0 |

Checking the shape of Dataframe

dataset.shape

(150000, 12)

Check the data types

dataset.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 150000 entries, 0 to 149999

Data columns (total 12 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Unnamed: 0 150000 non-null int64

1 SeriousDlqin2yrs 150000 non-null int64

2 RevolvingUtilizationOfUnsecuredLines 150000 non-null float64

3 age 150000 non-null int64

4 NumberOfTime30-59DaysPastDueNotWorse 150000 non-null int64

5 DebtRatio 150000 non-null float64

6 MonthlyIncome 120269 non-null float64

7 NumberOfOpenCreditLinesAndLoans 150000 non-null int64

8 NumberOfTimes90DaysLate 150000 non-null int64

9 NumberRealEstateLoansOrLines 150000 non-null int64

10 NumberOfTime60-89DaysPastDueNotWorse 150000 non-null int64

11 NumberOfDependents 146076 non-null float64

dtypes: float64(4), int64(8)

memory usage: 13.7 MB

Observation: All Columns are Numeric, either int or float

Check for Missing Values

dataset.isnull().sum()

Unnamed: 0 0

SeriousDlqin2yrs 0

RevolvingUtilizationOfUnsecuredLines 0

age 0

NumberOfTime30-59DaysPastDueNotWorse 0

DebtRatio 0

MonthlyIncome 29731

NumberOfOpenCreditLinesAndLoans 0

NumberOfTimes90DaysLate 0

NumberRealEstateLoansOrLines 0

NumberOfTime60-89DaysPastDueNotWorse 0

NumberOfDependents 3924

dtype: int64

Observation: There are two attributes missing some values, lets see the percentage missing.

dataset.isnull().sum() * 100 / len(df)

Unnamed: 0 0.000000

SeriousDlqin2yrs 0.000000

RevolvingUtilizationOfUnsecuredLines 0.000000

age 0.000000

NumberOfTime30-59DaysPastDueNotWorse 0.000000

DebtRatio 0.000000

MonthlyIncome 19.820667

NumberOfOpenCreditLinesAndLoans 0.000000

NumberOfTimes90DaysLate 0.000000

NumberRealEstateLoansOrLines 0.000000

NumberOfTime60-89DaysPastDueNotWorse 0.000000

NumberOfDependents 2.616000

dtype: float64

dataset.nunique()

Unnamed: 0 150000

SeriousDlqin2yrs 2

RevolvingUtilizationOfUnsecuredLines 125728

age 86

NumberOfTime30-59DaysPastDueNotWorse 16

DebtRatio 114194

MonthlyIncome 13594

NumberOfOpenCreditLinesAndLoans 58

NumberOfTimes90DaysLate 19

NumberRealEstateLoansOrLines 28

NumberOfTime60-89DaysPastDueNotWorse 13

NumberOfDependents 13

dtype: int64

dataset.duplicated().value_counts()

False 150000

dtype: int64

dataset['Unnamed: 0'].describe()

count 150000.000000

mean 75000.500000

std 43301.414527

min 1.000000

25% 37500.750000

50% 75000.500000

75% 112500.250000

max 150000.000000

Name: Unnamed: 0, dtype: float64

Observation: This is just the index field or unique row number , which will not add any value to the modeling. so lets drop it.

dataset.drop(columns = ['Unnamed: 0'], axis=1, inplace = True)

dataset.duplicated().value_counts()

False 149391

True 609

dtype: int64

dataset = dataset.drop_duplicates()

dataset.shape

(149391, 11)

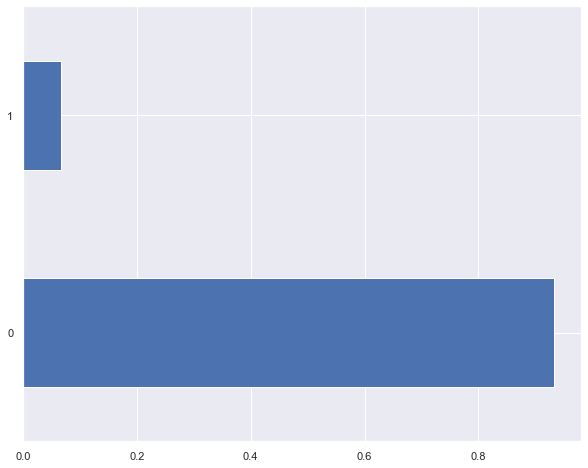

Now lets see how our labels are distributed

dataset['SeriousDlqin2yrs'].value_counts(normalize= True)

0 0.933001

1 0.066999

Name: SeriousDlqin2yrs, dtype: float64

df['SeriousDlqin2yrs'].value_counts(normalize=True).plot(kind='barh');

Observation: We have roughly 93% NOT Delinquient, and only 7% customers are delinquent. This is classic example of CLASS IMBALANCE.

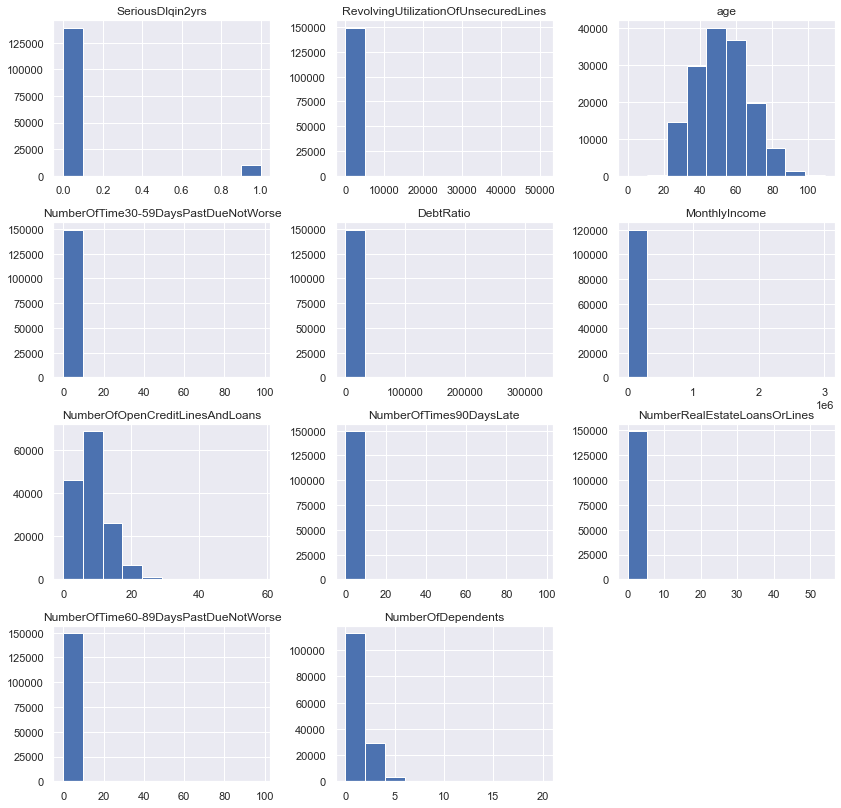

UNIVARIATE ANALYSIS - ONE VARIABLE AT A TIME

## UNIVARIATE ANALYSIS

# Creating histograms

dataset.hist(figsize=(14,14))

plt.show()

dataset['RevolvingUtilizationOfUnsecuredLines'].describe()

count 149391.000000

mean 6.071087

std 250.263672

min 0.000000

25% 0.030132

50% 0.154235

75% 0.556494

max 50708.000000

Name: RevolvingUtilizationOfUnsecuredLines, dtype: float64

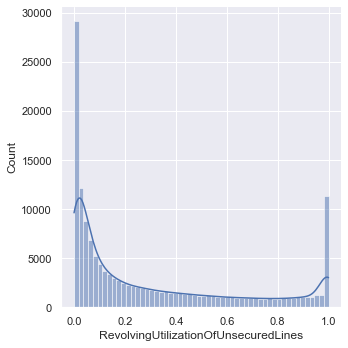

Observation: The max value is questionable. The revolving utilization means ratio of credit balance/ credit limit, which should always be 0 to 1, since it is ratio. Now lets see how many of such values we have.

len(dataset[(dataset['RevolvingUtilizationOfUnsecuredLines']>1)])

3321

## Lets see distribution of values that are <= 1

dataset_revUtil_less_than_one= dataset.loc[dataset['RevolvingUtilizationOfUnsecuredLines'] <=1]

sns.displot(data= dataset_revUtil_less_than_one, x= "RevolvingUtilizationOfUnsecuredLines", kde= True);

## since there are 3321 values have issues, its better to treat them as Nulls first and then impute, we can try ffill

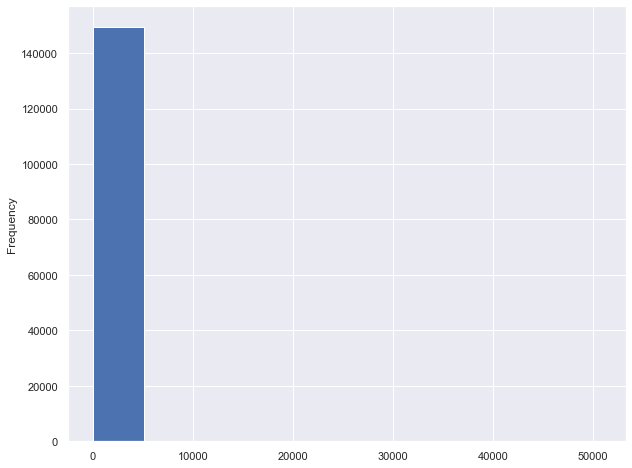

dataset['RevolvingUtilizationOfUnsecuredLines'] = dataset['RevolvingUtilizationOfUnsecuredLines'].map(lambda x: np.NaN if x >1 else x)

dataset['RevolvingUtilizationOfUnsecuredLines'].fillna(method='ffill', inplace=True)

dataset['RevolvingUtilizationOfUnsecuredLines'].describe()

count 149391.000000

mean 6.071087

std 250.263672

min 0.000000

25% 0.030132

50% 0.154235

75% 0.556494

max 50708.000000

Name: RevolvingUtilizationOfUnsecuredLines, dtype: float64

dataset['RevolvingUtilizationOfUnsecuredLines'].plot.hist();

We are able to change all the data into 0 to 1 range.

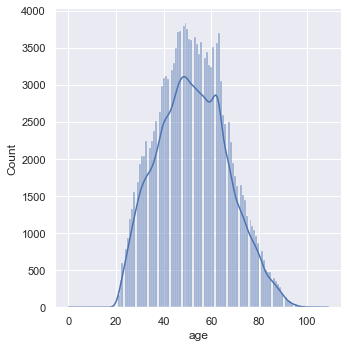

Age

dataset['age'].describe()

count 149391.000000

mean 52.306237

std 14.725962

min 0.000000

25% 41.000000

50% 52.000000

75% 63.000000

max 109.000000

Name: age, dtype: float64

sns.displot(data = dataset['age'], kde= True);

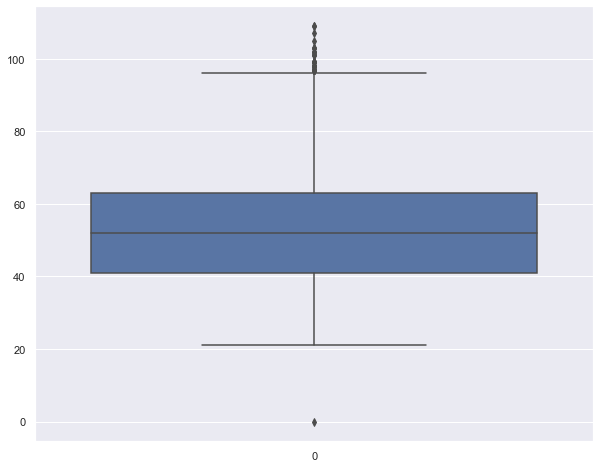

sns.boxplot(data= dataset['age'])

<AxesSubplot:>

Using Z Score for Outlier Analysis

dataset['age_zscore'] = (dataset['age'] - dataset['age'].mean())/dataset['age'].std(ddof=0)

dataset.head()

| SeriousDlqin2yrs | RevolvingUtilizationOfUnsecuredLines | age | NumberOfTime30-59DaysPastDueNotWorse | DebtRatio | MonthlyIncome | NumberOfOpenCreditLinesAndLoans | NumberOfTimes90DaysLate | NumberRealEstateLoansOrLines | NumberOfTime60-89DaysPastDueNotWorse | NumberOfDependents | age_zscore | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0.766127 | 45 | 2 | 0.802982 | 9120.0 | 13 | 0 | 6 | 0 | 2.0 | -0.496148 |

| 1 | 0 | 0.957151 | 40 | 0 | 0.121876 | 2600.0 | 4 | 0 | 0 | 0 | 1.0 | -0.835686 |

| 2 | 0 | 0.658180 | 38 | 1 | 0.085113 | 3042.0 | 2 | 1 | 0 | 0 | 0.0 | -0.971501 |

| 3 | 0 | 0.233810 | 30 | 0 | 0.036050 | 3300.0 | 5 | 0 | 0 | 0 | 0.0 | -1.514761 |

| 4 | 0 | 0.907239 | 49 | 1 | 0.024926 | 63588.0 | 7 | 0 | 1 | 0 | 0.0 | -0.224518 |

dataset[(dataset['age_zscore'] > 3) | (df['age_zscore'] < -3)].shape

(45, 12)

condition= dataset[(dataset['age_zscore'] > 3) | (dataset['age_zscore'] < -3)]

dataset.drop(condition.index, inplace= True)

df.shape

(149346, 12)

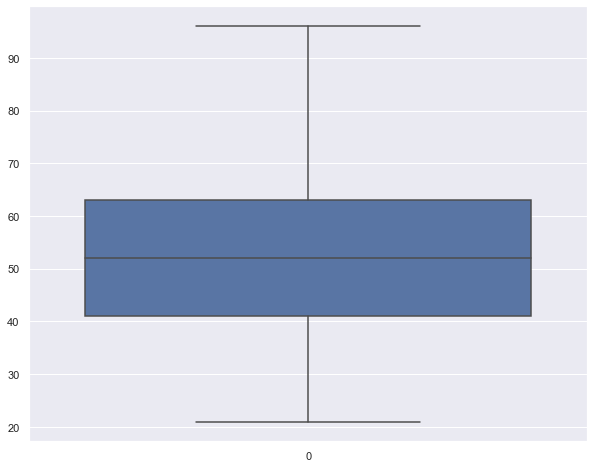

sns.boxplot(data= dataset['age'])

<AxesSubplot:>

dataset['age'].describe()

count 149346.000000

mean 52.292689

std 14.705177

min 21.000000

25% 41.000000

50% 52.000000

75% 63.000000

max 96.000000

Name: age, dtype: float64

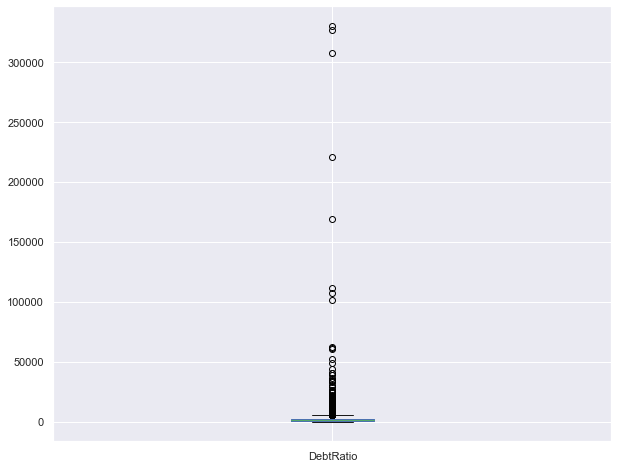

DEBT RATIO

Debt to income ratio or debt to assets ratio. This is typically 0 to 1, but sometimes it can be higher than 1, meaning person has more debt than income or assets.

dataset['DebtRatio'].describe()

count 149346.000000

mean 354.501212

std 2042.133602

min 0.000000

25% 0.177484

50% 0.368253

75% 0.875062

max 329664.000000

Name: DebtRatio, dtype: float64

dataset2=dataset[dataset['DebtRatio']>1]['DebtRatio']

dataset2

6 5710.000000

8 46.000000

14 477.000000

16 2058.000000

25 1.595253

...

149976 60.000000

149977 349.000000

149984 25.000000

149992 4132.000000

149997 3870.000000

Name: DebtRatio, Length: 35115, dtype: float64

dataset2.describe()

count 35115.000000

mean 1506.721853

std 4000.145613

min 1.000500

25% 42.000000

50% 908.500000

75% 2211.000000

max 329664.000000

Name: DebtRatio, dtype: float64

dataset2.plot.box()

<AxesSubplot:>

Lets make an assumption that Debt to Income ratio should be 0 to 1. Since there are 35,122 data points with Debt ratio higher than 1, instead of dropping them we can make assumption that number with higher than 1 are 100 % Debt ratio so fill them with 1.

dataset['DebtRatio']= dataset['DebtRatio'].apply(lambda x: 1 if x>1 else x)

dataset['DebtRatio']

0 0.802982

1 0.121876

2 0.085113

3 0.036050

4 0.024926

...

149995 0.225131

149996 0.716562

149997 1.000000

149998 0.000000

149999 0.249908

Name: DebtRatio, Length: 149346, dtype: float64

df['DebtRatio'].plot.hist()

<AxesSubplot:ylabel='Frequency'>

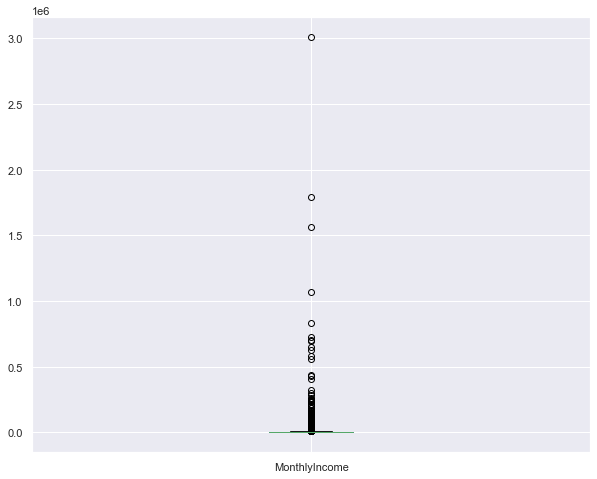

INCOME

dataset.MonthlyIncome.describe()

count 1.201470e+05

mean 6.675649e+03

std 1.439086e+04

min 0.000000e+00

25% 3.400000e+03

50% 5.400000e+03

75% 8.250000e+03

max 3.008750e+06

Name: MonthlyIncome, dtype: float64

dataset.MonthlyIncome.isnull().sum()

29199

dataset.MonthlyIncome.median()

5400.0

dataset['MonthlyIncome'].fillna(dataset['MonthlyIncome'].median(),inplace=True)

dataset.MonthlyIncome.plot.box()

<AxesSubplot:>

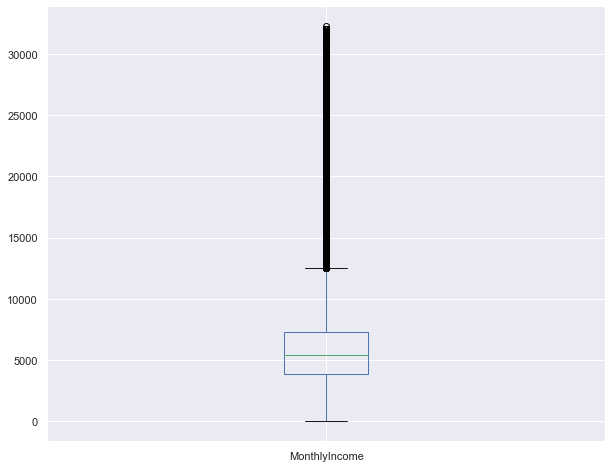

dataset['MonthlyIncome_zscore'] = (dataset['MonthlyIncome'] - dataset['MonthlyIncome'].mean())/dataset['MonthlyIncome'].std(ddof=0)

condition= dataset[(dataset['MonthlyIncome_zscore'] > 2) | (dataset['MonthlyIncome_zscore'] < -2)]

condition.shape

(704, 13)

dataset.drop(condition.index, inplace= True)

dataset.shape

(148642, 13)

dataset.MonthlyIncome.plot.box()

<AxesSubplot:>

dataset.MonthlyIncome.describe()

count 148642.000000

mean 6089.029790

std 3775.044698

min 0.000000

25% 3900.000000

50% 5400.000000

75% 7333.000000

max 32250.000000

Name: MonthlyIncome, dtype: float64

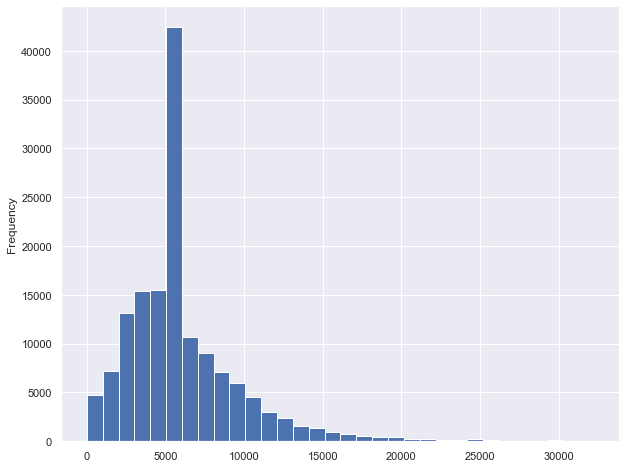

## If we want bin size of 1000 ,

bins = int((dataset.MonthlyIncome.max() - dataset.MonthlyIncome.min()) / 1000)

print(bins)

32

dataset.MonthlyIncome.plot.hist(bins=bins)

<AxesSubplot:ylabel='Frequency'>

There are 3 columns giving us information about Late Payments, lets look into them , one at a time.

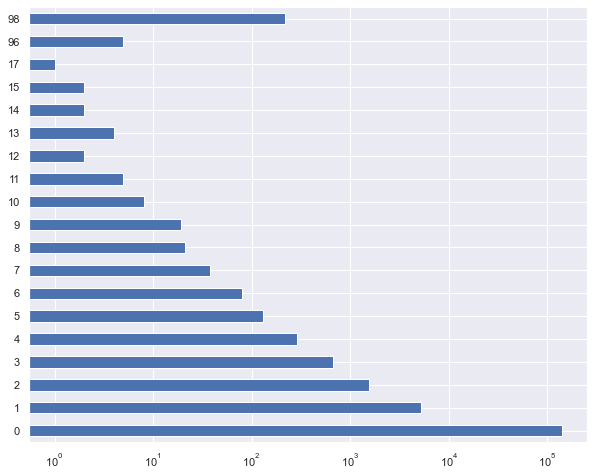

dataset["NumberOfTimes90DaysLate"].value_counts().sort_index()

0 140389

1 5211

2 1551

3 663

4 291

5 130

6 80

7 38

8 21

9 19

10 8

11 5

12 2

13 4

14 2

15 2

17 1

96 5

98 220

Name: NumberOfTimes90DaysLate, dtype: int64

plt.xscale('log') ## this is to visualize better if not in log scale it is heavily skewed

dataset["NumberOfTimes90DaysLate"].value_counts().sort_index().plot(kind= 'barh')

<AxesSubplot:>

dataset["NumberOfTime60-89DaysPastDueNotWorse"].value_counts().sort_index()

0 141111

1 5706

2 1116

3 317

4 104

5 34

6 16

7 9

8 2

9 1

11 1

96 5

98 220

Name: NumberOfTime60-89DaysPastDueNotWorse, dtype: int64

dataset["NumberOfTime30-59DaysPastDueNotWorse"].value_counts().sort_index()

0 124823

1 15953

2 4574

3 1744

4 745

5 341

6 138

7 54

8 25

9 12

10 4

11 1

12 2

13 1

96 5

98 220

Name: NumberOfTime30-59DaysPastDueNotWorse, dtype: int64

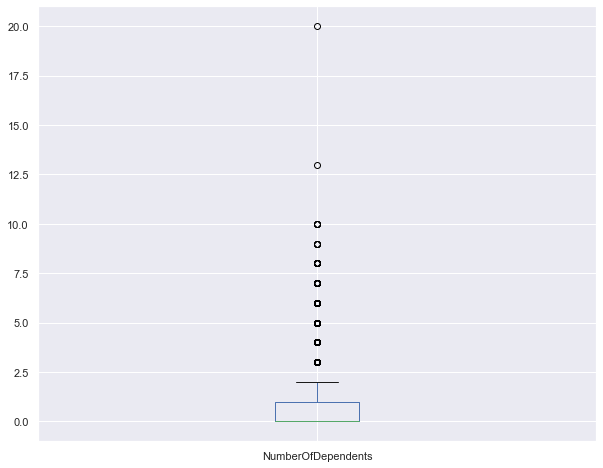

dataset["NumberOfDependents"].describe()

count 144827.000000

mean 0.757338

std 1.114128

min 0.000000

25% 0.000000

50% 0.000000

75% 1.000000

max 20.000000

Name: NumberOfDependents, dtype: float64

dataset["NumberOfDependents"].isnull().sum()

3815

dataset["NumberOfDependents"].plot.box()

<AxesSubplot:>

dataset['NumberOfDependents'].median()

0.0

# IMPUTE

dataset['NumberOfDependents'].fillna(dataset['NumberOfDependents'].median(),inplace=True)

dataset["NumberOfDependents"].isnull().sum()

0

BI-VARIATE ANALYSIS - TWO VARIABLES AT A TIME

SeriousDlqin2yrs Vs. RevolvingUtilizationOfUnsecuredLines

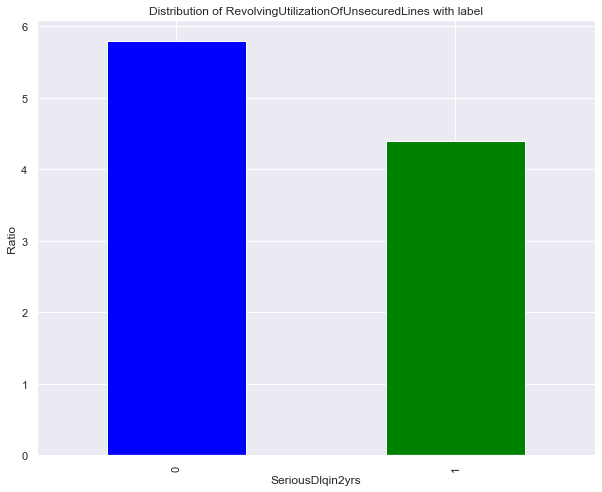

dataset['RevolvingUtilizationOfUnsecuredLines'].groupby(dataset.SeriousDlqin2yrs).mean().plot(kind='bar', color=['blue', 'green'])

plt.ylabel('Ratio')

plt.title('Distribution of RevolvingUtilizationOfUnsecuredLines with label')

Text(0.5, 1.0, 'Distribution of RevolvingUtilizationOfUnsecuredLines with label')

Observation: Delinquent customers got almost twice the utilization of unsecured lines

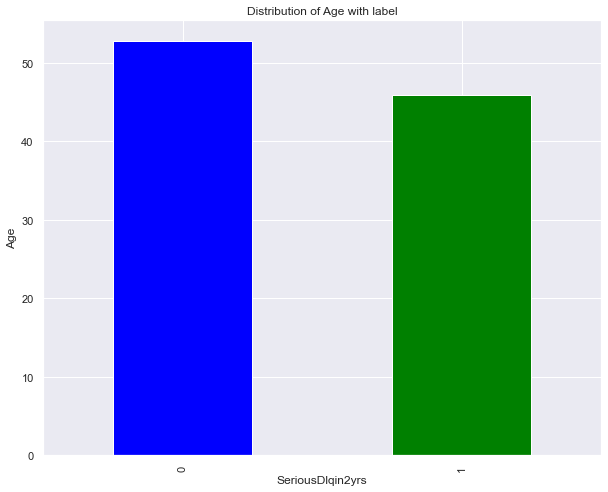

SeriousDlqin2yrs Vs. Age

dataset['age'].groupby(dataset.SeriousDlqin2yrs).mean().plot(kind='bar', color=['blue', 'green'])

plt.ylabel('Age')

plt.title('Distribution of Age with label')

Text(0.5, 1.0, 'Distribution of Age with label')

Observation: On average lower aged customers are more delinquent

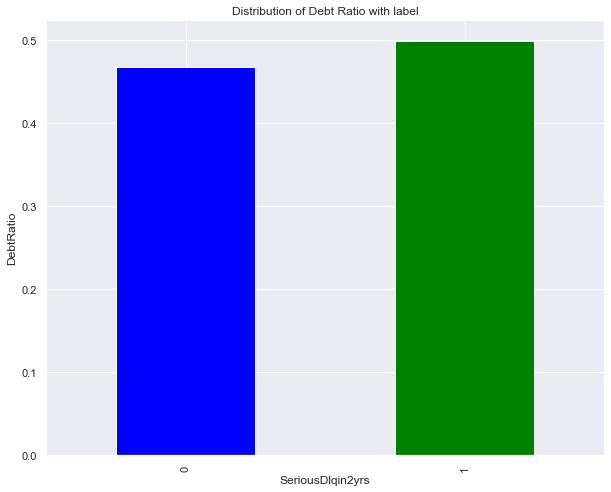

SeriousDlqin2yrs Vs. DebtRatio

dataset['DebtRatio'].groupby(dataset.SeriousDlqin2yrs).mean().plot(kind='bar', color=['blue', 'green'])

plt.ylabel('DebtRatio')

plt.title('Distribution of Debt Ratio with label')

Text(0.5, 1.0, 'Distribution of Debt Ratio with label')

Observation: ??? Ask to Class

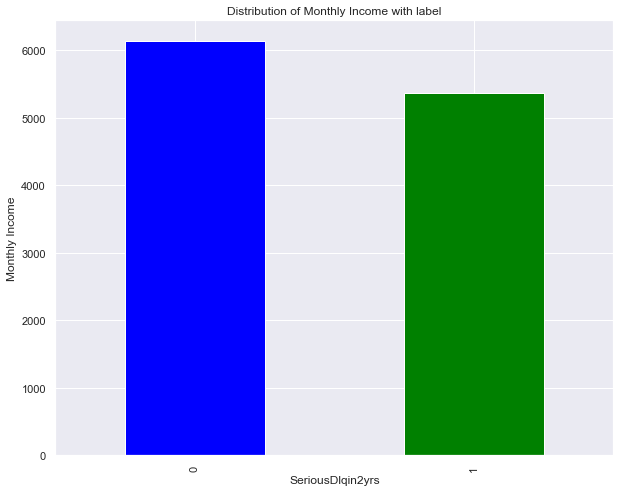

SeriousDlqin2yrs Vs. MonthlyIncome

dataset['MonthlyIncome'].groupby(dataset.SeriousDlqin2yrs).mean().plot(kind='bar', color=['blue', 'green'])

plt.ylabel('Monthly Income')

plt.title('Distribution of Monthly Income with label')

Text(0.5, 1.0, 'Distribution of Monthly Income with label')

Observation: ??? Ask to Class

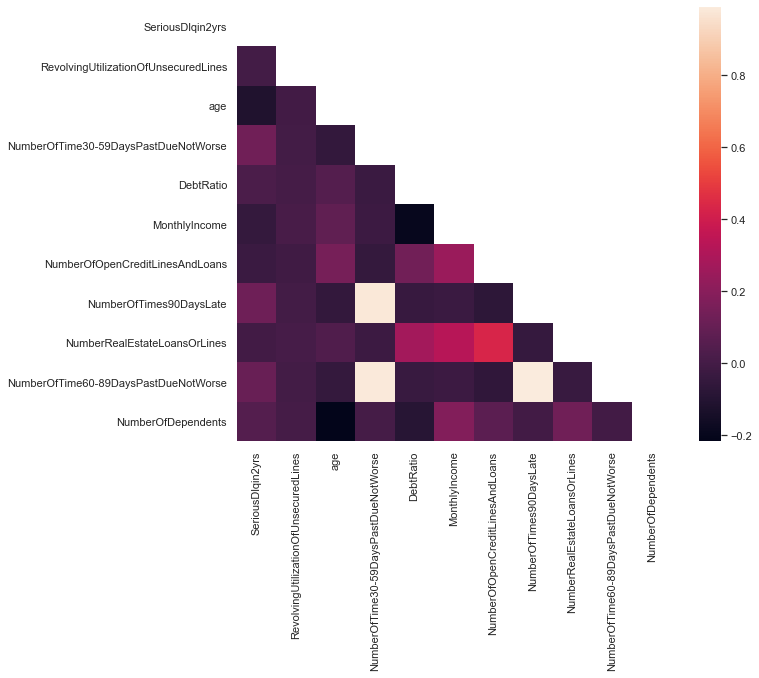

MULTI VARIATE ANALYSIS - more than two variables at a time, we will do correlation heatmap for this.

## First lets drop the z_score columns we create to remove outliers

dataset=dataset.drop(['age_zscore', 'MonthlyIncome_zscore'], axis=1)

dataset.columns

Index(['SeriousDlqin2yrs', 'RevolvingUtilizationOfUnsecuredLines', 'age',

'NumberOfTime30-59DaysPastDueNotWorse', 'DebtRatio', 'MonthlyIncome',

'NumberOfOpenCreditLinesAndLoans', 'NumberOfTimes90DaysLate',

'NumberRealEstateLoansOrLines', 'NumberOfTime60-89DaysPastDueNotWorse',

'NumberOfDependents'],

dtype='object')

corr = dataset.corr()

#sns.heatmap(corr) # simple but shows more noisy plot, adding mask to only see half is better

mask = np.zeros_like(corr)

mask[np.triu_indices_from(mask)] = True

with sns.axes_style("white"):

f, ax = plt.subplots(figsize=(10, 8))

ax = sns.heatmap(corr, mask=mask, square=True)

above figure shows that age and SeriousDlqin2yrs are highly correlated similarly NumberOfTimes90DaysLate and NumberOfTime30-59DaysPastDueNotWorse are less correlated. In the same way we can estimate the relationship between different attributes.

FEATURE ENGINEERING

What are some of the additional features we can create or drive from given attributes?

- We have monthly income and total dependents, we can derive income per person

- We have Debt to Income ratio so we can get total debt

- From 1 & 2, we can get monthly balance

- We can also sum all the dues , 30- 59 days, 60- 89 days, and 90 days

Let’s add these 4 new features for now.

# Income per person

dataset['Income_per_person'] = dataset['MonthlyIncome']/(dataset['NumberOfDependents']+1)

# Monthly Debt

dataset['Monthly_debt'] = dataset['DebtRatio']*dataset['MonthlyIncome']

# Monthly Balance

dataset['Monthly_balance'] = dataset['MonthlyIncome'] - dataset['Monthly_debt']

# Total number of DUEs

dataset['Total_number_of_dues'] = dataset['NumberOfTime30-59DaysPastDueNotWorse']+dataset['NumberOfTime60-89DaysPastDueNotWorse']+dataset['NumberOfTimes90DaysLate']

dataset.head()

| SeriousDlqin2yrs | RevolvingUtilizationOfUnsecuredLines | age | NumberOfTime30-59DaysPastDueNotWorse | DebtRatio | MonthlyIncome | NumberOfOpenCreditLinesAndLoans | NumberOfTimes90DaysLate | NumberRealEstateLoansOrLines | NumberOfTime60-89DaysPastDueNotWorse | NumberOfDependents | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0.766127 | 45 | 2 | 0.802982 | 9120.0 | 13 | 0 | 6 | 0 | 2.0 |

| 1 | 0 | 0.957151 | 40 | 0 | 0.121876 | 2600.0 | 4 | 0 | 0 | 0 | 1.0 |

| 2 | 0 | 0.658180 | 38 | 1 | 0.085113 | 3042.0 | 2 | 1 | 0 | 0 | 0.0 |

| 3 | 0 | 0.233810 | 30 | 0 | 0.036050 | 3300.0 | 5 | 0 | 0 | 0 | 0.0 |

| 5 | 0 | 0.213179 | 74 | 0 | 0.375607 | 3500.0 | 3 | 0 | 1 | 0 | 1.0 |

MODEL BUILDING

Before we start modeling, we need to make sure what evaluation metrics to use. Since we have imbalanced data set, we will be using Precision- Recall, and f1-score for evaluation.

Class 1: (YES) : Delinquent Customers Class 2: (NO): Non- Delinquent Customers

Here Class of Interest is positive class- which is Class 1. Lets discuss what could be more costly for business- whether False Positives or False Negatives.

If we predict customers will delinquent, but they are not. This means False Positives, because we falsely predicted positive class.

If we predict customers will NOT delinquent, but in reality they did. This means False Negatives, because we falsely predicted negative class.

From bank’s perspective, False Negative is more costly, because we miss to predict the customers who will delinquent. Since False Negatives matter more, we should aim to reduce FNs, that means RECALL will be more important that PRECISION.

Precision = TP / TP + FP

Recall = TP / TP + FN

Steps to follow:

- Split the data into train and test set (lets take 70-30 split)

- Scale the data ( also called normalize): we can pick StandardScaler or MinMaxScaler

- Try 3 different models: Logistic Regression, RandomForest, XGBoost

- Compare the evaluation metrics

- Pick the best performing and generalized model

## TRAIN AND TEST SPLIT 70 to 30 percent

X = dataset.drop(columns=['SeriousDlqin2yrs'])

y = dataset['SeriousDlqin2yrs']

X_train, X_test, y_train, y_test = train_test_split(X, y,stratify= y,random_state=42,shuffle=True,test_size=0.3)

print('Shape of training data', X_train.shape)

print('-'*40)

print('Shape of test data', X_test.shape)

print('-'*40)

Shape of training data (104049, 10)

----------------------------------------

Shape of test data (44593, 10)

----------------------------------------

## SCALE THE DATA, we will use standard scaler

sc= StandardScaler()

X_train_scaled=sc.fit_transform(X_train)

X_train_scaled=pd.DataFrame(X_train_scaled, columns=X.columns)

# Transform on test data

X_test_scaled=sc.transform(X_test)

X_test_scaled=pd.DataFrame(X_test_scaled, columns=X.columns)

X_train_scaled.head()

| RevolvingUtilizationOfUnsecuredLines | age | NumberOfTime30-59DaysPastDueNotWorse | DebtRatio | MonthlyIncome | NumberOfOpenCreditLinesAndLoans | NumberOfTimes90DaysLate | NumberRealEstateLoansOrLines | NumberOfTime60-89DaysPastDueNotWorse | NumberOfDependents | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | -0.027215 | 1.475614 | -0.102208 | -1.283644 | 0.112021 | -0.289289 | -0.062012 | -0.912388 | -0.055610 | 0.239036 |

| 1 | -0.027219 | 0.386825 | -0.102208 | -1.137202 | -0.183511 | 0.099620 | -0.062012 | -0.912388 | -0.055610 | -0.666237 |

| 2 | -0.023049 | -0.429767 | -0.102208 | -0.397614 | 0.367459 | -0.094834 | 0.201595 | -0.015583 | 0.209069 | 1.144309 |

| 3 | -0.024338 | 0.727071 | 0.159529 | 1.496206 | -0.183511 | 0.294075 | -0.062012 | -0.015583 | -0.055610 | -0.666237 |

| 4 | -0.025999 | 1.067318 | -0.102208 | 0.137173 | -0.285739 | -0.483743 | -0.062012 | 0.881221 | -0.055610 | -0.666237 |

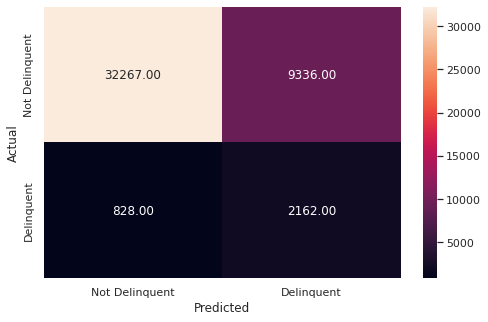

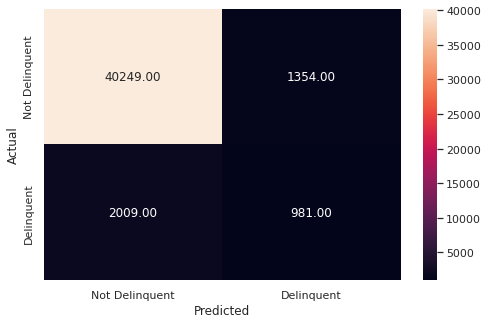

# Creating metric function

# Metrics to evaluate the model

def metrics_score(actual, predicted):

print(classification_report(actual, predicted))

cm = confusion_matrix(actual, predicted)

plt.figure(figsize=(8,5))

sns.heatmap(cm, annot=True, fmt='.2f', xticklabels=['Not Delinquent', 'Delinquent'], yticklabels=['Not Delinquent', 'Delinquent'])

plt.ylabel('Actual')

plt.xlabel('Predicted')

plt.show()

X_train_scaled.isnull().sum()

RevolvingUtilizationOfUnsecuredLines 0

age 0

NumberOfTime30-59DaysPastDueNotWorse 0

DebtRatio 0

MonthlyIncome 0

NumberOfOpenCreditLinesAndLoans 0

NumberOfTimes90DaysLate 0

NumberRealEstateLoansOrLines 0

NumberOfTime60-89DaysPastDueNotWorse 0

NumberOfDependents 0

dtype: int64

# Fitting logistic regression model

lg=LogisticRegression(random_state=42, class_weight='balanced')

lg.fit(X_train_scaled,y_train)

LogisticRegression(class_weight='balanced', random_state=42)

# Checking the performance on the training data

y_pred_train = lg.predict(X_train_scaled)

metrics_score(y_train, y_pred_train)

precision recall f1-score support

0 0.97 0.79 0.87 97071

1 0.19 0.66 0.29 6978

accuracy 0.78 104049

macro avg 0.58 0.72 0.58 104049

weighted avg 0.92 0.78 0.83 104049

# Checking the performance on the test dataset

y_pred_test = lg.predict(X_test_scaled)

metrics_score(y_test, y_pred_test)

precision recall f1-score support

0 0.97 0.78 0.86 41603

1 0.19 0.72 0.30 2990

accuracy 0.77 44593

macro avg 0.58 0.75 0.58 44593

weighted avg 0.92 0.77 0.83 44593

# Printing the coefficients of logistic regression

cols=X.columns

coef_lg=lg.coef_

pd.DataFrame(coef_lg,columns=cols).T.sort_values(by = 0,ascending = False)

| 0 | |

|---|---|

| NumberOfTimes90DaysLate | 2.297865 |

| NumberOfTime30-59DaysPastDueNotWorse | 2.134538 |

| NumberOfTime60-89DaysPastDueNotWorse | 0.543397 |

| NumberOfDependents | 0.097003 |

| DebtRatio | 0.094698 |

| NumberRealEstateLoansOrLines | 0.062493 |

| NumberOfOpenCreditLinesAndLoans | 0.011010 |

| RevolvingUtilizationOfUnsecuredLines | -0.012984 |

| MonthlyIncome | -0.147554 |

| age | -0.450574 |

# Predict_proba gives the probability of each observation belonging to each class

y_scores_lg=lg.predict_proba(X_train_scaled)

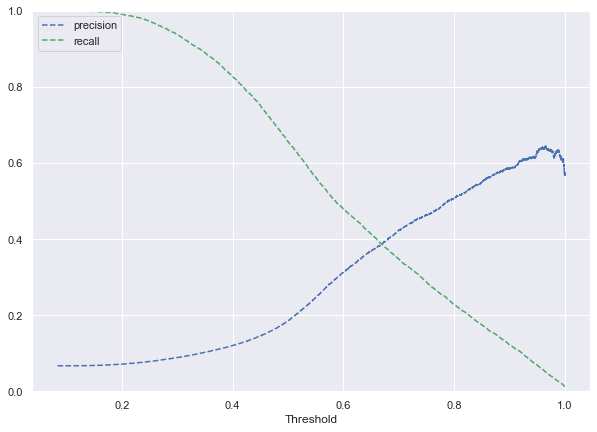

precisions_lg, recalls_lg, thresholds_lg = precision_recall_curve(y_train, y_scores_lg[:,1])

# Plot values of precisions, recalls, and thresholds

plt.figure(figsize=(10,7))

plt.plot(thresholds_lg, precisions_lg[:-1], 'b--', label='precision')

plt.plot(thresholds_lg, recalls_lg[:-1], 'g--', label = 'recall')

plt.xlabel('Threshold')

plt.legend(loc='upper left')

plt.ylim([0,1])

plt.show()

## Intersection of Precision and Recall is Optimum threshold

optimal_threshold=.78

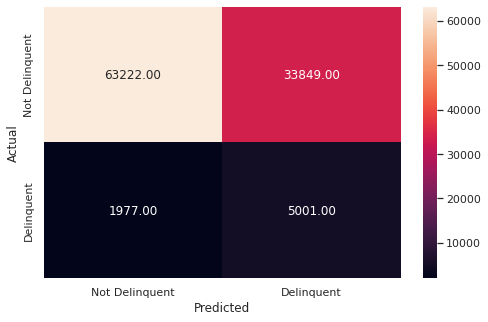

y_pred_train = lg.predict_proba(X_train_scaled)

metrics_score(y_train, y_pred_train[:,1]>optimal_threshold)

precision recall f1-score support

0 0.95 0.98 0.96 97071

1 0.49 0.25 0.33 6978

accuracy 0.93 104049

macro avg 0.72 0.62 0.65 104049

weighted avg 0.92 0.93 0.92 104049

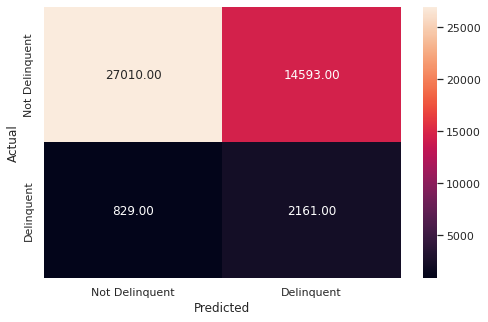

optimal_threshold=.78

y_pred_test = lg.predict_proba(X_test_scaled)

metrics_score(y_test, y_pred_test[:,1]>optimal_threshold)

precision recall f1-score support

0 0.95 0.97 0.96 41603

1 0.42 0.33 0.37 2990

accuracy 0.92 44593

macro avg 0.69 0.65 0.66 44593

weighted avg 0.92 0.92 0.92 44593

Observation:

- The model is giving similar performance on the test and train data i.e. the model is giving a generalized performance.

- The precision of the test data has increased significantly while at the same time, the recall has decreased, which is to be expected while adjusting the threshold.

- Since RECALL is important for us as discussed abaove before we began model building, we CANNOT use higher threshold to lose the recall.

- The average recall and precision for the model are good but let’s see if we can get better performance using other algorithms.

Remember our goal is to have better Recall

# Fitting the Random Forest classifier on the training data

rf_estimator = RandomForestClassifier(class_weight = {0: 0.93, 1: 0.07}, random_state = 42) ## class weight comes from initial class distribution

rf_estimator.fit(X_train_scaled, y_train)

RandomForestClassifier(class_weight={0: 0.93, 1: 0.07}, random_state=42)

# Checking performance on the training data

y_pred_train_rf = rf_estimator.predict(X_train)

metrics_score(y_train, y_pred_train_rf)

precision recall f1-score support

0 0.97 0.65 0.78 97071

1 0.13 0.72 0.22 6978

accuracy 0.66 104049

macro avg 0.55 0.68 0.50 104049

weighted avg 0.91 0.66 0.74 104049

# Checking performance on the testing data

y_pred_test_rf = rf_estimator.predict(X_test)

metrics_score(y_test, y_pred_test_rf)

precision recall f1-score support

0 0.97 0.65 0.78 41603

1 0.13 0.72 0.22 2990

accuracy 0.65 44593

macro avg 0.55 0.69 0.50 44593

weighted avg 0.91 0.65 0.74 44593

Comments